Executive Summary

This report presents a comprehensive financial viability assessment of Hampshire County Council (HCC) as of February 2026. It has been commissioned to evaluate the Authority’s funding outlook, quantify potential shortfalls over the medium term (2026-2031), analyze the root causes of the prevailing fiscal distress, and interrogate the contingency measures currently in place. Furthermore, the report provides a forensic analysis of expenditure trends to answer the critical stakeholder question: “Where has the money gone?”

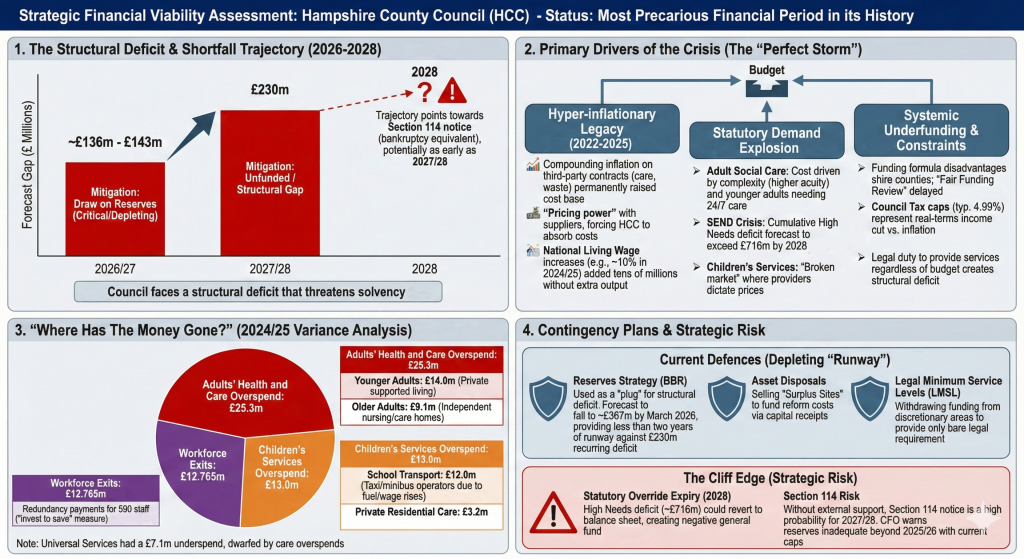

The analysis indicates that Hampshire County Council is currently navigating the most precarious financial period in its history. Despite a longstanding reputation for prudent fiscal management and a reserve position that historically exceeded the national average 1, the Council faces a structural deficit that threatens its solvency within the current Medium Term Financial Strategy (MTFS) period.

As of the 2026/27 budget setting process, the unmitigated budget shortfall stands at approximately £136 million to £143 million.2 This gap is projected to widen to £230 million by 2027/28 2, creating a trajectory that, without external intervention or radical structural change, points towards the issuance of a Section 114 notice—the local government equivalent of bankruptcy—potentially as early as the 2027/28 financial year.2

The drivers of this crisis are multifaceted but can be categorized into three primary vectors:

- Hyper-inflationary Legacy (2022-2025): The compounding effect of inflation on third-party contracts (particularly in care and waste) has permanently raised the cost base beyond the capacity of Council Tax and Business Rates to compensate.5

- Statutory Demand Explosion: There has been an unprecedented surge in demand for high-cost statutory services, specifically Adult Social Care (complex needs in younger adults) and Special Educational Needs and Disabilities (SEND), where the cumulative deficit is forecast to exceed £716 million by 2028.7

- Systemic Underfunding: The delay in the “Fair Funding Review” and the structural disadvantage of the current funding formula for shire counties have left HCC with a core spending power that is insufficient to meet its legal duties.6

Contingency planning is now heavily reliant on “one-off” measures. The Council is balancing its 2026/27 budget primarily through a massive drawdown of its Budget Bridging Reserve (BBR), a strategy acknowledged by the Chief Financial Officer (CFO) as unsustainable.2 Other contingencies include the “Savings Programme 2026” (SP26), aggressive asset disposals under the “Surplus Sites” programme 9, and requests for Exceptional Financial Support (EFS) from central government to bypass Council Tax referendum limits.2

The following report details these findings, providing a rigorous examination of the financial data, strategic risks, and operational realities facing Hampshire County Council.

1. Macro-Fiscal Context and Strategic Environment

To understand the specific shortfalls facing Hampshire County Council, one must first situate the Authority within the broader macro-fiscal environment of the mid-2020s. The financial distress observed is not an isolated phenomenon but the result of a collision between rigid local government finance structures and a dynamic, inflationary global economy.

1.1 The “Perfect Storm” of 2022-2025

The period leading up to the 2026/27 budget was characterized by economic volatility that fundamentally altered the cost base of local government. Unlike the private sector, which can adjust pricing dynamically, local authorities are constrained by annual tax setting cycles and capped revenue streams.

- Inflationary Hysteresis: While headline Consumer Price Index (CPI) inflation began to stabilize by late 2025, the level of prices had permanently shifted upwards. For HCC, this “hysteresis” effect meant that the cost of building roads, heating schools, and purchasing care beds had risen by 20-30% over three years, while funding had increased by significantly less. The “pricing power” lay entirely with suppliers (care homes, construction firms, waste processors), forcing the Council to absorb these costs.6

- The National Living Wage (NLW) Impact: The substantial increases in the NLW, particularly the near 10% rise in 2024/25, acted as a massive external shock. HCC is a major commissioner of labor-intensive services (domiciliary care, cleaning, school catering). When the statutory wage floor rises, the Council must increase the fees paid to external providers to prevent market failure. This “pass-through” inflation added tens of millions to the recurring budget without generating any additional service output.10

- Interest Rate Environment: The Bank of England’s base rate adjustments throughout 2024 and 2025 5 impacted the cost of borrowing for capital projects. While HCC’s treasury management strategy successfully mitigated some risks through fixed-rate borrowing, the cost of new debt for infrastructure projects (e.g., the new Material Recycling Facility) became significantly more expensive, squeezing the revenue budget further.11

1.2 The Funding Formula Imbalance

A critical element of the shortfall is the structural inequity in how central government allocates resources. HCC argues that the current formula fails to recognize the specific cost drivers of large shire counties.

- The “Shire Penalty”: County councils typically receive less funding per resident than metropolitan boroughs or unitary cities, despite having higher costs for services like transport (due to rurality) and social care (due to older populations). HCC has lobbied extensively that “needs are not being correctly assessed,” leading to resources being directed away from areas with genuine demographic pressures.12

- Fair Funding Review Delays: The long-promised “Fair Funding Review,” intended to recalibrate these inequities, has been repeatedly delayed. The “Fair Funding Review 2.0” consultation in mid-2025 6 introduced further uncertainty, with initial modelling suggesting HCC could actually lose a further £15.9 million in funding—a “disappointing” outcome that forced the Council to budget for the worst-case scenario.3

1.3 The Reserve Position: A Depleting Shield

Historically, HCC maintained high reserve levels compared to the national average, a fact often cited by critics as evidence of “hoarding.” However, the events of 2023-2026 have vindicated the CFO’s prudence. These reserves have acted as a shock absorber, allowing the Council to avoid the immediate Section 114 notices issued by other authorities (e.g., Birmingham, Nottingham).

However, this shield is now dangerously thin. The strategy of using the “Budget Bridging Reserve” (BBR) to smooth the transition between savings programs has been replaced by a necessity to use reserves to fund day-to-day operations. As the CFO noted in the Section 25 report, “reserves alone would not sustain long-term balance,” and the current trajectory of drawdowns is unsustainable.2

2. Financial Forecast: Shortfalls and Funding Gaps (2026-2031)

The user’s query specifically asks for the potential shortfalls over the coming 3-5 years. The data from the Medium Term Financial Strategy (MTFS) paints a picture of widening structural deficits that grow exponentially rather than linearly.

2.1 The 2026/27 Budget Gap

As of February 2026, the Council is finalizing the budget for the 2026/27 financial year. The figures reveal a significant unmitigated shortfall.

- Gross Budget Gap: The gap between required expenditure and forecast income was initially projected at £143 million in the November 2025 update.2 Following the provisional Local Government Finance Settlement (LGFS) in December 2025, this was revised slightly downwards to £136 million.3

- Drivers of the 2026/27 Gap:

- Inflation: Non-pay inflation added approximately £10 million to the requirement.

- Adult Social Care: New pressure of £13.9 million due to complexity and volume growth.

- Funding Reduction: A confirmed reduction in government grant funding of £9.2 million (better than the feared £15.9m, but still a cut).3

- Balancing Mechanism: This £136 million gap is not being closed by new savings. Instead, it is being plugged primarily by a draw from the Budget Bridging Reserve. This is a critical distinction: the structural deficit remains; it is merely being cash-flowed for another 12 months.

2.2 The 2027/28 Cliff Edge

The outlook for the subsequent year, 2027/28, is significantly bleaker. The forecast budget gap jumps to £230 million.2

- Why the Jump? The jump is caused by the depletion of “one-off” mitigations used in 2026/27. When reserves are used to pay for recurring costs (like staff salaries or care home fees), the hole reappears the following year, often larger due to inflation.

- Reserve Exhaustion: By the end of 2026/27, the BBR is forecast to be heavily depleted. The CFO has explicitly stated that reserves “are not adequate in the overall context of the financial position beyond the 2025/26 financial year” if Council Tax is capped at 4.99%.13 This implies that without a change in trajectory, the Council will not have the cash resources to cover the £230 million gap in 2027/28.

2.3 Medium-Term Outlook (2028-2031)

Extrapolating beyond 2028 involves significant uncertainty but follows a clear trendline of deterioration based on the Council’s “structural deficit” model.

- Structural Deficit: The Council estimates a recurring deficit of approximately £200 million per annum.4 This means that every year, the cost of standing still rises faster than income by this amount.

- Statutory Override Expiry (2028): A critical milestone is 31 March 2028. This is the date the government’s statutory override for the Dedicated Schools Grant (DSG) deficit expires. At this point, the accumulated High Needs deficit (forecast to be £716 million) would theoretically revert to the Council’s balance sheet.7

- Insolvency Risk: If this override expires without a solution, HCC would effectively have a negative general fund balance of hundreds of millions of pounds. Under the Local Government Finance Act 1988, this would legally oblige the CFO to issue a Section 114 notice immediately.

Table 1: Forecast Budget Shortfalls (2025-2028)

| Financial Year | Forecast Gap (Unmitigated) | Primary Mitigation Strategy | Status of Reserves |

| 2025/26 | £116.2m | Draw on Reserves (£64.9m) + SP25 Savings | Adequate for year only 14 |

| 2026/27 | £136.0m – £143.0m | Draw on Reserves + SP26 Savings (£2.6m) | Critical / Depleting 2 |

| 2027/28 | £230.0m | Unfunded / Structural Gap | Insufficient 2 |

3. Analysis of Causation: Why is there a Shortfall?

The user asks, “Why is there a potential shortfall?” The answer is not simply “lack of money” but a complex interplay of demographic shifts, market failures, and rigid statutory obligations. HCC is legally required to provide services for which it is not adequately funded.

3.1 Adult Social Care: The Demographic Timebomb

Adult Social Care (ASC) is the largest single consumer of the Council’s discretionary budget. The shortfall here is driven by a shift in the nature of demand, not just volume.

- Complexity over Volume: While the number of older people is rising, the cost is driven by complexity. Residents entering care homes today have higher acuity needs (e.g., advanced dementia, multiple comorbidities) than a decade ago. This requires higher staffing ratios in care homes, pushing up the weekly fee HCC must pay.

- Younger Adults (Learning Disabilities): This is the area of highest risk and growth. Medical advances mean children with severe disabilities are surviving into adulthood and living longer. These individuals often require 24/7 one-to-one care. The cost of a single package can exceed £4,000 per week. The “Younger Adults” budget has seen consistent overspends (e.g., £14.0m pressure in 2024/25) because the budget cannot keep pace with the number of young people transitioning from Children’s Services.15

- Market Fragility: The care market in Hampshire is fragile. Providers face their own inflationary pressures (energy, food, wages). If HCC does not pay sustainable rates, providers hand back contracts, forcing the Council to spot-purchase care at emergency (and significantly higher) rates.

3.2 Children’s Services: A Broken Market

The market for children’s residential care is described by sector experts as “broken.” Demand for placements for children with complex behavioural needs vastly outstrips supply.

- The “Profiteering” Problem: Because there is a shortage of secure beds, private providers can dictate prices. HCC has seen the cost of placements spiral, leading to an £18.0 million growth requirement for “Children Looked After” in the 2026/27 budget.7

- Unaccompanied Asylum Seeking Children (UASC): Hampshire, as a county with ports and proximity to entry points, supports a high number of UASC. While the Home Office provides a daily rate, it often falls short of the actual cost of supporting older adolescents with trauma and complex needs. The 2024/25 outturn showed a £5.8 million pressure specifically for UASC.15

3.3 The SEND Crisis (High Needs Block)

Perhaps the single largest driver of the “hidden” deficit is the explosion in Special Educational Needs and Disabilities (SEND) costs.

- The Legislative Trigger: The Children and Families Act 2014 extended the age range for SEND support to 25. This created a “double cohort” of young people entitled to support without commensurate funding.

- EHCP Growth: Between 2018 and 2025, the number of Education, Health and Care Plans (EHCPs) in Hampshire grew by nearly 80%.2

- Transport Costs: There is a direct causal link between EHCPs and transport costs. If a child is placed in a special school 20 miles away, the Council must transport them. This has caused School Transport costs to balloon, with a £12.0 million pressure reported in 2024/25.15

- The Deficit Loop: The government grant (High Needs Block) is insufficient to cover these costs. HCC spends more than it receives, creating an annual deficit of ~£140m. This deficit sits in a negative reserve, creating the “cliff edge” mentioned in Section 2.3

3.4 Regulatory and Policy Constraints

The shortfall is also a product of what the Council is not allowed to do.

- Council Tax Capping: HCC is generally limited to a 4.99% Council Tax increase (2.99% general + 2% ASC precept). With inflation running at 10% in some sectors, this represents a real-terms cut in income. The Council’s request to raise tax by 14.99% to close the gap was rejected by central government, effectively locking in the shortfall.13

- Statutory Duties: The Council cannot legally turn away an eligible child or vulnerable adult. It must provide the service regardless of whether it has the budget. This disconnect between legal duty and financial capacity is the definition of the structural deficit.

4. Expenditure Analysis: Where Has the Money Gone?

To answer the user’s specific question regarding the destination of funds (“where has the money gone”), this section provides a forensic analysis of expenditure during the 2024/25 and 2025/26 periods. It counters the narrative that money has been “wasted” and instead illustrates how it has been absorbed by the rising unit costs of statutory provision.

4.1 Directorate Outturn Analysis (2024/25)

The 2024/25 financial outturn provides the clearest evidence of expenditure flows. The Authority reported a net underspend of £5.6 million, but this masks significant underlying overspends in key areas.15

Adults’ Health and Care: £25.3m Overspend

The “money” in this directorate has primarily flowed to the private social care market.

- Private Care Providers: The £25.3m overspend was not on internal bureaucracy but on fees paid to independent nursing homes and domiciliary care agencies.

- Unit Cost Inflation: The daily cost of a nursing bed rose significantly.

- Care Home Improvement Programme (CHIP): £5.3 million was spent on revenue costs associated with this programme, which could no longer be capitalized. This represents money spent on modernizing care delivery that hit the revenue bottom line.15

Children’s Services: £13.0m Overspend

The expenditure here is dominated by transport and external placements.

- The Taxi Economy: A staggering £12.0 million overspend occurred in School Transport. This money went to local taxi firms, minibus operators, and transport escorts. The rise in fuel prices and driver wages (driven by the logistics labor shortage) meant HCC paid significantly more for the same number of journeys.15

- Private Residential Care: The £3.2m pressure in social care went to private providers of children’s homes, often located out-of-county due to a lack of local provision.

Universal Services: £7.1m Underspend

Interestingly, money was saved in the Universal Services directorate (Highways, Waste).

- Contract Management: Efficiencies were achieved in the waste disposal contract (Veolia) and highways maintenance. This demonstrates that where the Council has control over specifications (e.g., reducing frequency of grass cutting or rationalizing waste operations), it can control costs. However, this saving was dwarfed by the overspends in care.

4.2 Workforce Rationalization Costs

A significant sum has been spent on reducing the size of the organization.

- Exit Packages: In the 2024/25 financial year, HCC paid out £12.765 million in redundancy and exit packages to 590 staff.16

- Rationale: While this appears as a large expenditure (“money gone”), it is an “invest to save” measure. By spending £12.7m one-off, the Council removes the recurring salary costs of those 590 posts from future budgets. The payback period is typically less than two years.

- Funding Source: Critically, this was largely funded through the “flexible use of capital receipts” (selling buildings to pay for redundancies), thereby protecting the revenue budget for services.

4.3 Capital Expenditure vs. Revenue

It is crucial to distinguish between revenue (day-to-day) and capital (building stuff).

- Capital Programme: In 2024/25, £259 million was spent on capital projects.15 This money went into physical assets: building new schools (e.g., North Whiteley), maintaining 5,000 miles of roads, and upgrading bridges.

- Debt Servicing: The Council holds roughly £250 million in debt.17 A portion of the revenue budget goes to paying interest on this debt. However, compared to other authorities (e.g., Portsmouth at £682m), HCC’s debt burden is low. The “money” is not disappearing into debt interest; it is disappearing into the operating costs of social care.

Table 2: Where the Money Went (2024/25 Variance Analysis)

| Cost Center | Variance (Overspend) | Destination of Funds |

| Adults: Younger Adults | £14.0m | Private providers of supported living for learning disabilities |

| Adults: Older Adults | £9.1m | Independent nursing and residential care homes |

| Children: School Transport | £12.0m | Taxi, minibus, and private transport operators |

| Children: UASC/Looked After | £3.2m | Private residential care providers (out-of-county) |

| Workforce Exits | £12.7m | Redundancy payments to 590 departing staff 16 |

5. Contingency Plans and Mitigation Strategies

The user explicitly asks: “what contingency plans are in place?” HCC has developed a layered defence strategy, ranging from operational efficiencies to strategic asset liquidation and political lobbying.

5.1 The “Savings Programmes” (SP25 & SP26)

Hampshire operates on a biennial savings cycle. These are the primary mechanism for reducing the structural deficit.

- Savings Programme to 2025 (SP25): This program aimed to deliver £134.1 million in recurring savings. Measures included digital transformation, restructuring management tiers, and reducing discretionary grants. As of early 2026, the majority of this has been delivered, though slippage in some complex areas (e.g., social care transformation) required reserve cover.3

- Savings Programme 2026 (SP26): Recognized as an interim “bridge,” SP26 targets a modest £2.6 million in additional savings for 2026/27.11 The small scale of this program acknowledges that the “low hanging fruit” has long been harvested. Further cuts would essentially require breaching statutory duties.

- Specific Measures: Reductions in the Parish Lengthsman scheme (£50k), decommissioning illuminated street furniture to save energy (£25k), and increasing income targets for Hampshire Transport Management.11

5.2 The Reserves Strategy: The “Runway”

The most critical contingency is the use of the Budget Bridging Reserve (BBR).

- Mechanism: The BBR was designed to hold surpluses from previous years to smooth out the timing differences between cost increases and savings delivery.

- Current Usage: It is now being used as a “plug” for the structural deficit.

- 2024/25 Draw: £68.5m.

- 2025/26 Draw: £64.9m.

- 2026/27 Forecast: ~£136m.

- Contingency Risk: The reserves are forecast to fall to £367 million by March 2026.2 While substantial in absolute terms, against a recurring deficit of £230m, this provides a “runway” of less than two years. Once this contingency is exhausted (projected 2027/28), the Council has no further internal financial buffer.

5.3 Asset Disposals: The “Surplus Sites” Strategy

To generate cash to fund transformation (and thus protect reserves), HCC has accelerated its property disposal programme.

- Strategy: Identify underutilized land and buildings (e.g., old depots, closed offices) and sell them for development.

- Jan 2026 Decision: The Executive Member for Hampshire 2050 approved a disposal strategy for multiple sites.9

- Flexible Use of Capital Receipts: Government rules allow capital receipts from these sales to be used to fund the revenue costs of reform (e.g., redundancy payments, IT investment). This is a vital contingency that prevents these one-off costs from hitting the general fund.

5.4 Legal Minimum Service Levels (LMSL)

A more controversial contingency is the rigorous application of “Legal Minimum Service Levels.”

- Concept: The Council has reviewed every service line to distinguish between what is statutorily required and what is discretionary.

- Implementation: Funding is being withdrawn from discretionary areas. For example, the Education Catering service was outsourced in 2026 to prevent it from running a deficit that subsidized school meals beyond the statutory requirement.7

- Impact: This contingency effectively redefines the social contract with residents, reducing the Council’s offer to the bare legal bone to ensure solvency.

5.5 Structural Reform: Local Government Reorganisation (LGR)

Looking beyond the immediate term, HCC has proposed a radical structural change as a contingency against long-term insolvency.

- The Proposal: The “Future Hampshire” plan proposes abolishing the current two-tier system (1 County Council + 11 District Councils) and replacing it with four new Unitary Authorities.18

- Financial Logic: This would eliminate the duplication of 12 Chief Executives, 12 Finance Directors, and 12 IT departments. HCC estimates this could save £50 million annually.18

- Status: This remains a proposal subject to government approval. Even if greenlit, savings would not be realized until post-2028, meaning it is not a solution for the immediate 2026/27 crisis.

6. Strategic Risk Assessment: The Section 114 Question

The ultimate question underpinning this entire analysis is the risk of insolvency.

6.1 The “Section 114” Mechanism

Under the Local Government Finance Act 1988, if a CFO concludes that the authority cannot balance its budget, they must issue a Section 114 notice. This freezes all non-statutory spending and triggers a period of government intervention (commissioners).

6.2 The CFO’s Assessment (February 2026)

In the Section 25 report accompanying the 2026/27 budget, the CFO provided a stark assessment:

- Current Status: HCC is not issuing a Section 114 notice for 2026/27. The ability to balance the budget via the BBR prevents this.4

- Future Risk: The CFO warned that adhering to the 4.99% Council Tax cap “increases the likelihood that the Council would issue a Section 114 notice… in advance of the 2026/27 financial year” (referring to the planning for the subsequent year).13

- The Verdict: The Council is solvent for now, but structurally unsound. It is “burning the furniture to keep the house warm.” Without a successful application for Exceptional Financial Support (raising tax by ~15%) or a government bailout of the High Needs Block, a Section 114 notice is a high probability event for the 2027/28 budget cycle.

7. Conclusion

Hampshire County Council is an authority operating at the limit of its financial elasticity. The potential shortfall of £136m in 2026/27 and £230m in 2027/28 is not a forecast of mismanagement but a reflection of a broken funding model for shire counties.

The “money has gone” into absorbing the hyper-inflation of the mid-2020s and meeting the legal rights of a growing population of vulnerable adults and children. Contingency plans are robust but finite; the “runway” provided by reserves will run out within 24 months.

Recommendations for Stakeholders:

- Expect Service Reductions: The move to Legal Minimum Service Levels will become increasingly visible to residents (e.g., reduced library hours, stricter care eligibility).

- Council Tax Volatility: Residents should anticipate continued attempts by the Council to breach the 4.99% cap via EFS requests, potentially leading to double-digit increases in future years.

- Structural Change: The status quo is untenable. Stakeholders should prepare for eventual Local Government Reorganisation or significant Devolution deals as the only viable long-term exit routes from this fiscal crisis.

The Council remains a going concern as of February 2026, but the warning lights are flashing red.

Appendix: Key Financial Data Summary

| Metric | Figure | Source |

| 2026/27 Unmitigated Budget Gap | £136.0m – £143.0m | 2 |

| 2027/28 Forecast Budget Gap | £230.0m | 2 |

| High Needs Cumulative Deficit (2028) | £716.0m (Forecast) | 7 |

| Workforce Exit Costs (2024/25) | £12.765m | 16 |

| Reserves (BBR) Forecast (March 2026) | ~£367.0m | 2 |

| Proposed SP26 Savings | £2.6m | 11 |

Works cited

- Decision – Medium Term Financial Strategy, accessed February 8, 2026, https://democracy.hants.gov.uk/ieDecisionDetails.aspx?Id=828

- Medium Term Financial Position – Meetings, agendas, and minutes – Hampshire County Council, accessed February 8, 2026, https://democracy.hants.gov.uk/documents/s140152/November%202025%20MTFS%20Update.pdf

- Executive Member for Hampshire 2050 and Corpora, accessed February 8, 2026, https://democracy.hants.gov.uk/documents/s142671/2%20Corporate%20Services%20Directorate%20DD%20Select%20FY2026-27%20Budget%20Reportv2.pdf

- Agenda item – Section 25 Report of the Chief Financial Officer, accessed February 8, 2026, https://democracy.hants.gov.uk/mgAi.aspx?ID=73301

- Appendix 12 Treasury Management Strategy 2025/26 Introduction – Meetings, agendas, and minutes – Hampshire County Council, accessed February 8, 2026, http://democracy.hants.gov.uk/documents/s130061/Appendix%2012%20-%20202526%20Treasury%20Management%20Strategy.pdf

- Medium Term Financial Position – Interim Update Report From – Meetings, agendas, and minutes – Hampshire County Council, accessed February 8, 2026, https://democracy.hants.gov.uk/documents/s135595/Item%208%20-%20Report%20-%20Medium%20Term%20Financial%20Strategy%20Update.pdf

- Executive Lead Member for Children’s Services Date: 21 January 2026 T – Hampshire County Council, accessed February 8, 2026, https://democracy.hants.gov.uk/documents/s142482/Executive%20Member%20report.pdf

- Budget and council tax 2025/26 | About the Council – Hampshire County Council, accessed February 8, 2026, https://www.hants.gov.uk/aboutthecouncil/budgetspendingandperformance/budgetandcounciltax

- Surplus Sites Programme/Disposal Strategy-2026-01-22-EMH2050 Decision Day – Hampshire County Council, accessed February 8, 2026, https://democracy.hants.gov.uk/documents/s143165/Decision%20Record.pdf

- 2024/25 Revenue Budget Report for Adults’ Health and Care Report …, accessed February 8, 2026, https://democracy.hants.gov.uk/documents/s115887/Revenue%20Budget%20Report%20for%20Adults%20Health%20and%20Care%20Decision%20Report.pdf

- 2026-27 US Revenue Budget and SP26 Savings-2026-01-19-ELMUS Decision Day – Meetings, agendas, and minutes – Hampshire County Council, accessed February 8, 2026, https://democracy.hants.gov.uk/documents/s142392/2026-27%20US%20Revenue%20Budget%20and%20SP26%20Savings.pdf

- Written evidence submitted by Hampshire County Council [FSF 0015] – UK Parliament Committees, accessed February 8, 2026, https://committees.parliament.uk/writtenevidence/135464/pdf/

- HAMPSHIRE COUNTY COUNCIL Executive Decision Record Decision Maker: Cabinet Date: 4 February 2025 Title: Section 25 Report from t, accessed February 8, 2026, https://democracy.hants.gov.uk/documents/s130703/Decision%20Record%20-%20sec%2025%20report.pdf

- Revenue Budget and Precept 2025/26 Report – Meetings, agendas, and minutes – Hampshire County Council, accessed February 8, 2026, https://democracy.hants.gov.uk/documents/s130058/2025-26%20Revenue%20Budget%20Report.pdf

- Corporate report template – Meetings, agendas, and minutes, accessed February 8, 2026, https://democracy.hants.gov.uk/documents/s135596/Item%207%20-%20Report%20-%20End%20of%20Year%20Financial%20Report%202024-25.pdf

- Hampshire County Council pays out £12.7m in redundancy payments – Daily Echo, accessed February 8, 2026, https://www.dailyecho.co.uk/news/25368754.hampshire-county-council-pays-12-7m-redundancy-payments/

- Council debt in Hampshire and Solent tops £2.7billion – Basingstoke Gazette, accessed February 8, 2026, https://www.basingstokegazette.co.uk/news/25423501.council-debt-hampshire-solent-tops-2-7billion/

- Shaping a stronger future – transforming local government across Hampshire and the Solent, accessed February 8, 2026, https://www.hants.gov.uk/News/20250926LGR_submission_to_Government

- Our proposal – four unitary councils – Hampshire County Council, accessed February 8, 2026, https://www.hants.gov.uk/aboutthecouncil/governmentinhampshire/future-hampshire-solent/local-government-reorganisation/proposal