1. Understanding the Phenomenon: The Mechanics of the 2026 Super El Niño

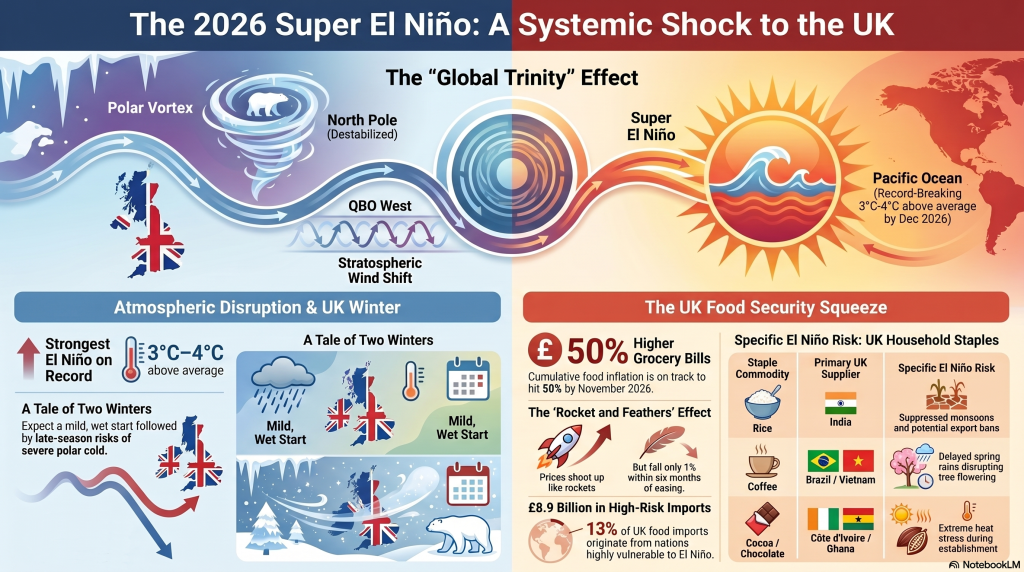

The El Niño Southern Oscillation (ENSO) is the primary driver of global climate variability, and for the United Kingdom’s interconnected economy, its current trajectory represents a critical strategic risk. While ENSO is a Pacific-based cycle, it acts as a “global circulation reset,” triggering a reorganization of atmospheric patterns that reset weather conditions thousands of miles away. Understanding these mechanics is essential for navigating the systemic shocks now entering the North Atlantic corridor.

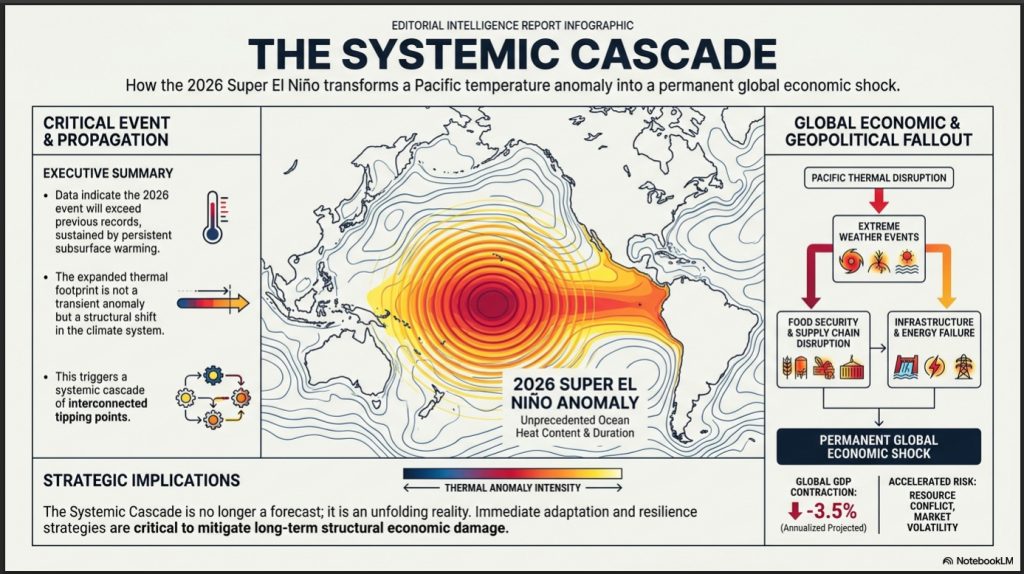

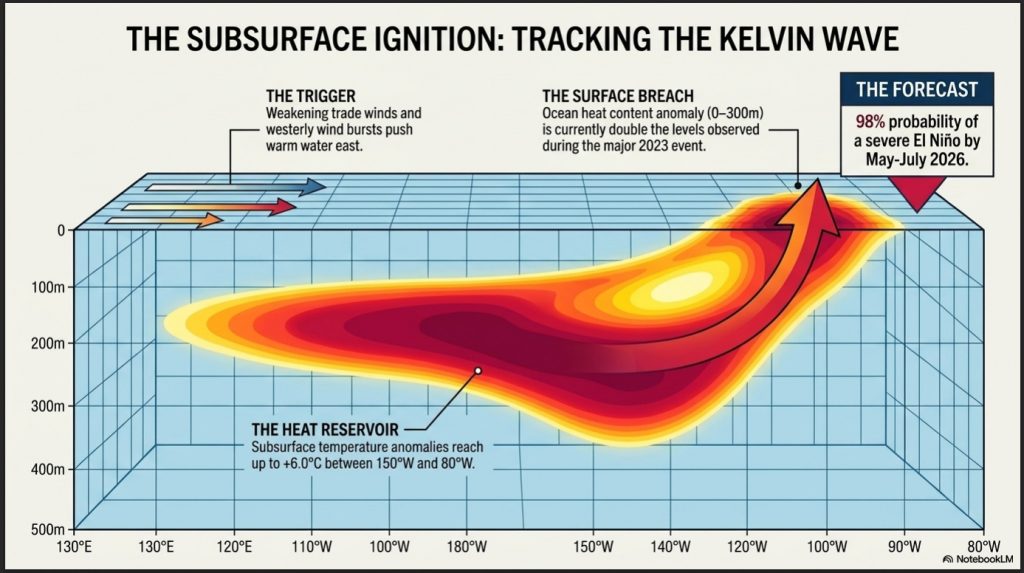

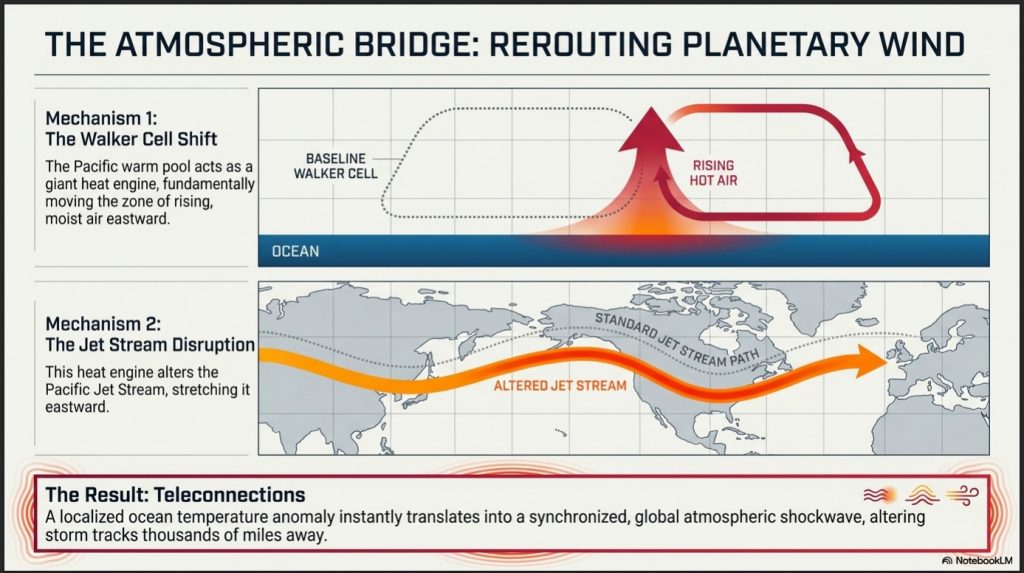

The 2026 event is characterized by a breakdown in the Walker Cell circulation. Typically, trade winds push warm surface water toward Asia, but a significant weakening—and in some regions, a reversal—of these winds has allowed a massive subsurface reservoir of heat to migrate eastward. This “Kelvin Wave,” driven by westerly wind bursts, is now surfacing in the eastern Pacific. As this energy is released into the atmosphere, it acts as a “pressure release valve” for years of accumulated oceanic heat, creating an “atmospheric bridge” that alters the global jet stream.

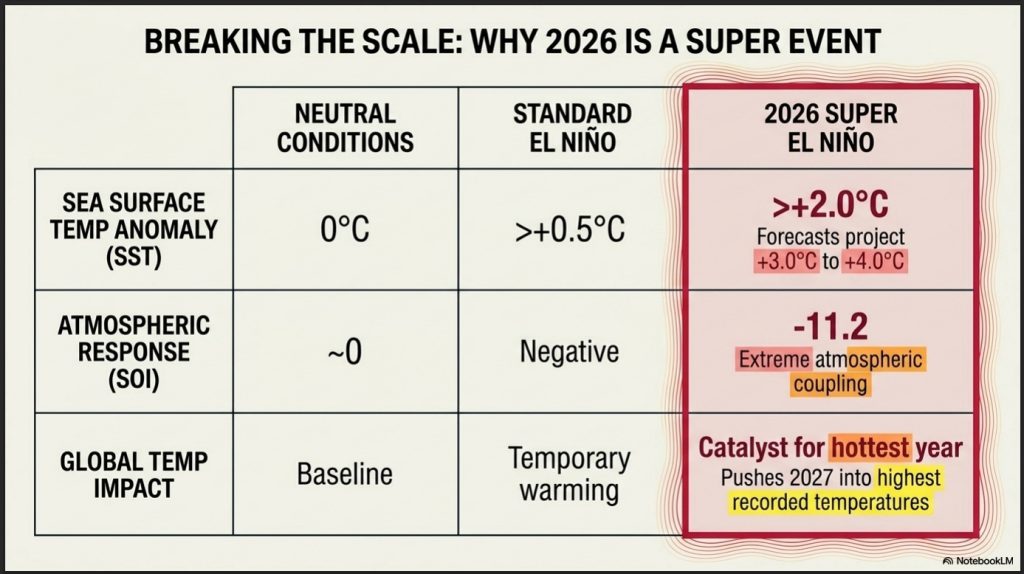

Current projections suggest the 2026 event will reach unprecedented severity, likely becoming the strongest El Niño in recorded history.

| Event Period | Peak Sea-Surface Temperature (SST) Anomaly | Severity Classification |

|---|---|---|

| 1997-1998 | +2.3°C | Strong / Super |

| 2015-2016 | +2.3°C | Strong / Super |

| 2026 (Projected) | +3.0°C to +4.0°C | Historic / Super El Niño |

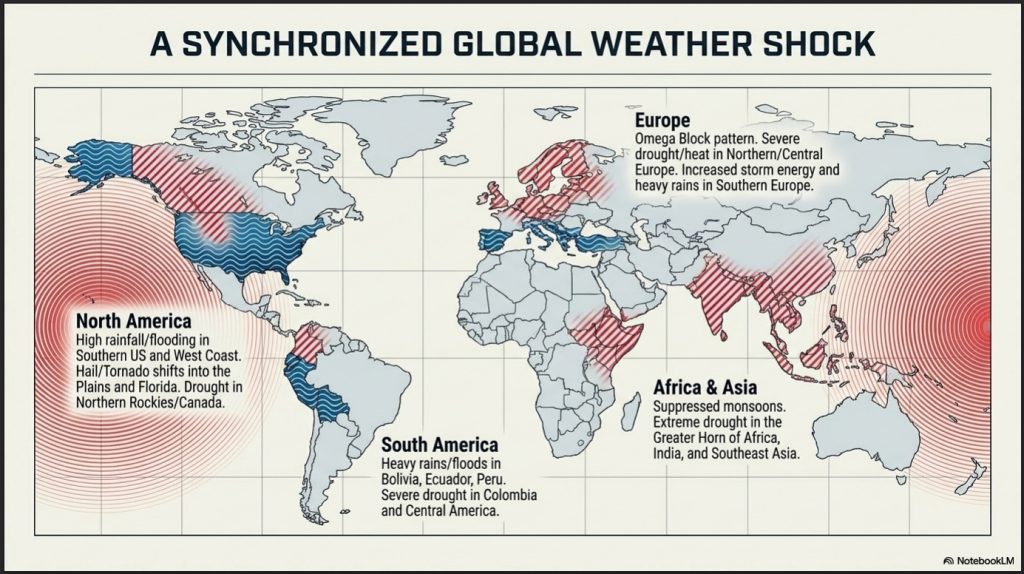

While the physical epicenter of this Kelvin Wave remains in the tropical Pacific, its energy is redistributed globally. This redistribution directly influences the North Atlantic storm tracks, ensuring that the physical shifts in the Pacific manifest as tangible volatility for the British Isles.

2. Meteorological Forecast: Projected Impacts on United Kingdom Weather Patterns

The United Kingdom’s geographical position makes it highly susceptible to indirect El Niño impacts. This occurs primarily through the alteration of the North Atlantic jet stream, the high-altitude “ribbon” of air that dictates the track and intensity of weather systems approaching Europe. Rather than the direct “weather whiplash” seen in the tropics, the UK experiences a reconfiguration of its seasonal volatility.

Based on projections from the Met Office and the National Centre for Atmospheric Science (NCAS), the 2026/2027 cycle presents a distinct meteorological timeline:

- Autumn and Early Winter: An increased likelihood of unsettled, milder, wetter, and windier conditions as the jet stream shifts into a more volatile, southerly configuration.

- Late Winter: A projected transition toward colder, calmer periods, which increases the risk of damaging frost following the preceding wet spells.

The strategic risk for the UK lies in the compounding nature of this volatility. The UK has already suffered three of the worst harvests on record in the past five years; a Super El Niño-driven winter of extreme rainfall followed by late-season freezing represents a catastrophic threat to domestic agricultural recovery. These domestic weather changes are, however, only half of the exposure, as the UK’s heavy reliance on international trade makes it a passive recipient of even more severe climate shocks occurring abroad.

3. Global Supply Chain Vulnerabilities: Risks to UK Food Distribution

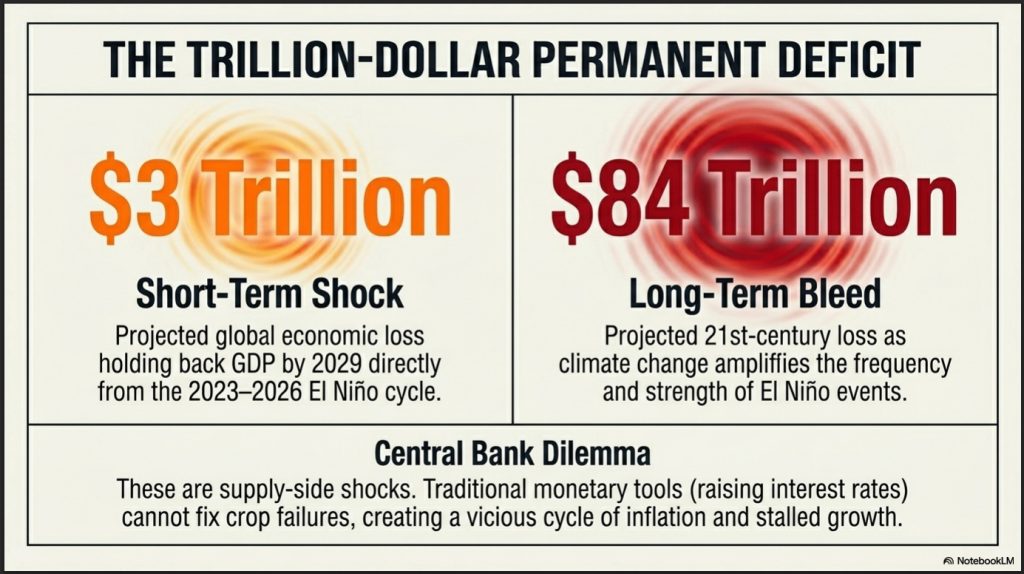

The United Kingdom imports approximately two-fifths of its food, a dependency that leaves the national supply chain vulnerable to external production shocks. The 2026 Super El Niño arrives during a period of extreme geopolitical instability, specifically the war in Iran, which has already caused soaring fuel and fertilizer prices. This conflict acts as a secondary shock, limiting the ability of global farmers to use high-input methods to compensate for climate-driven crop failures.

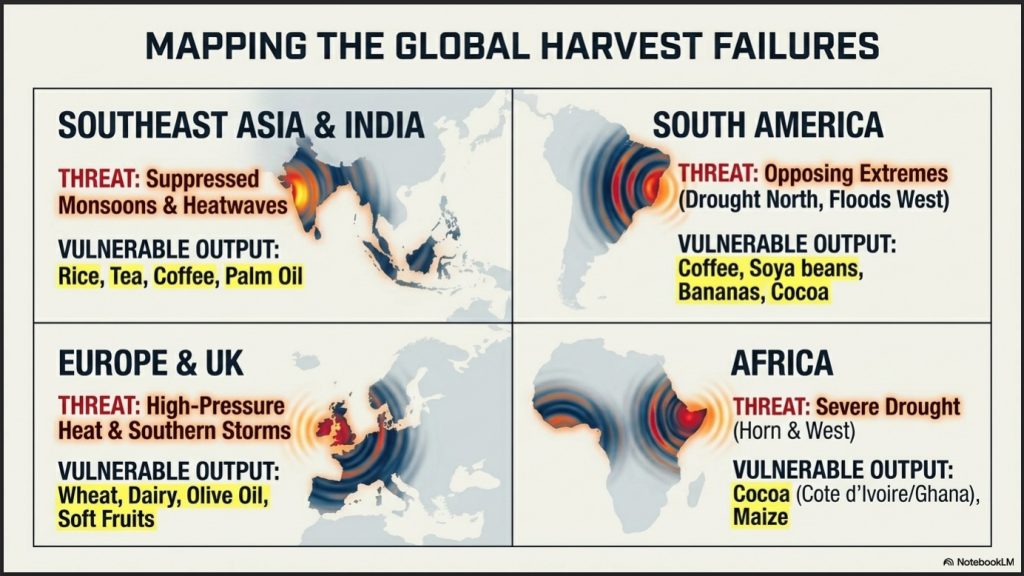

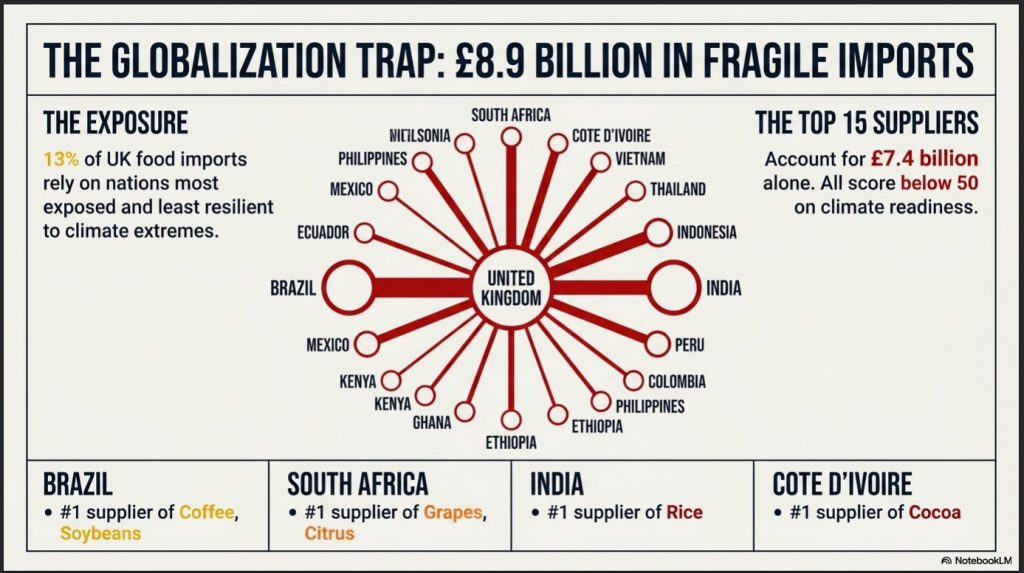

Currently, 13% of UK food imports—valued at £8.9 billion—originate from nations with high climate vulnerability. The “Top 15” suppliers from these regions, including South Africa (citrus and apples) and Egypt (grapes and strawberries), account for £7.4 billion in trade that is now at direct risk.

| UK Staple/Commodity | Primary Source Country | El Niño-Driven Threat | Impact on UK Supply Chain |

| Rice | India | Heat stress / Weakened monsoon | Primary source for UK domestic consumption |

| Maize & Soya | Argentina / Brazil | Severe drought / Heat stress | Critical animal feed for UK meat and dairy |

| Coffee | Brazil / Vietnam | Temperature spikes / Drought | Supply contraction from top two global producers |

| Cocoa | Côte d’Ivoire / Ghana | Irregular rain / Crop failure | Persistent price inflation in confectionary |

| Bananas | Colombia / Ecuador | Extreme rain and flooding | Disruption of high-volume, low-margin staple |

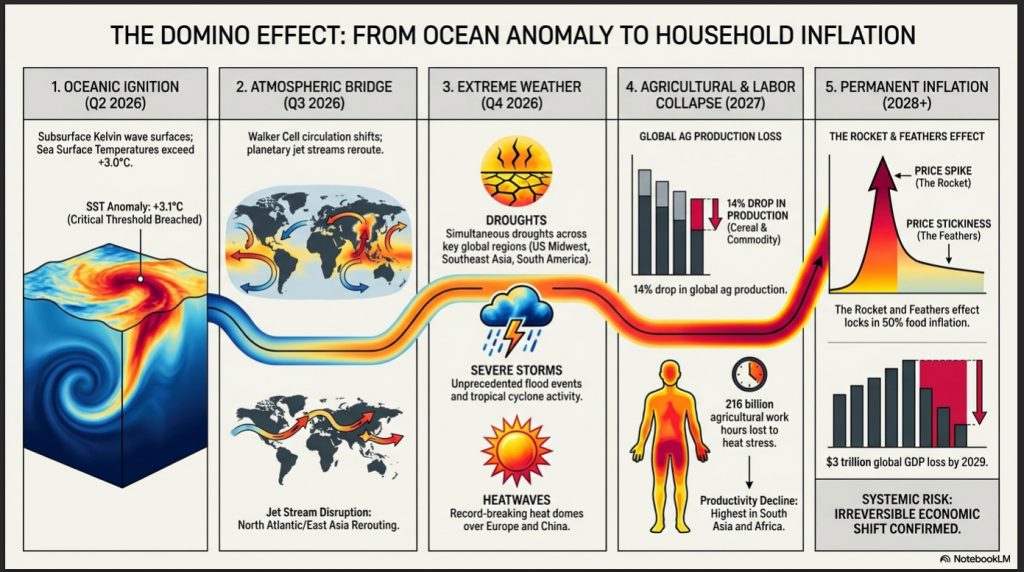

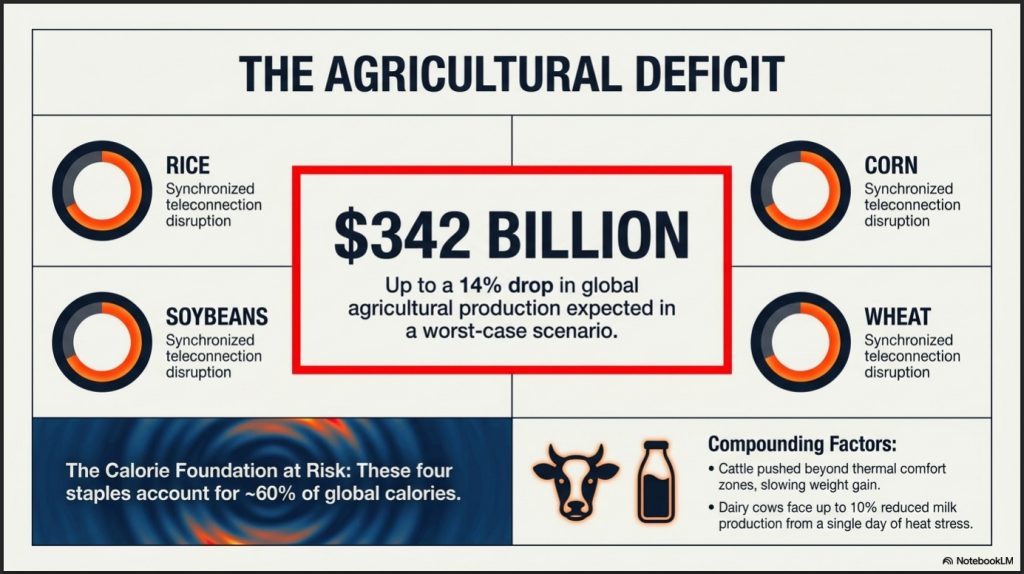

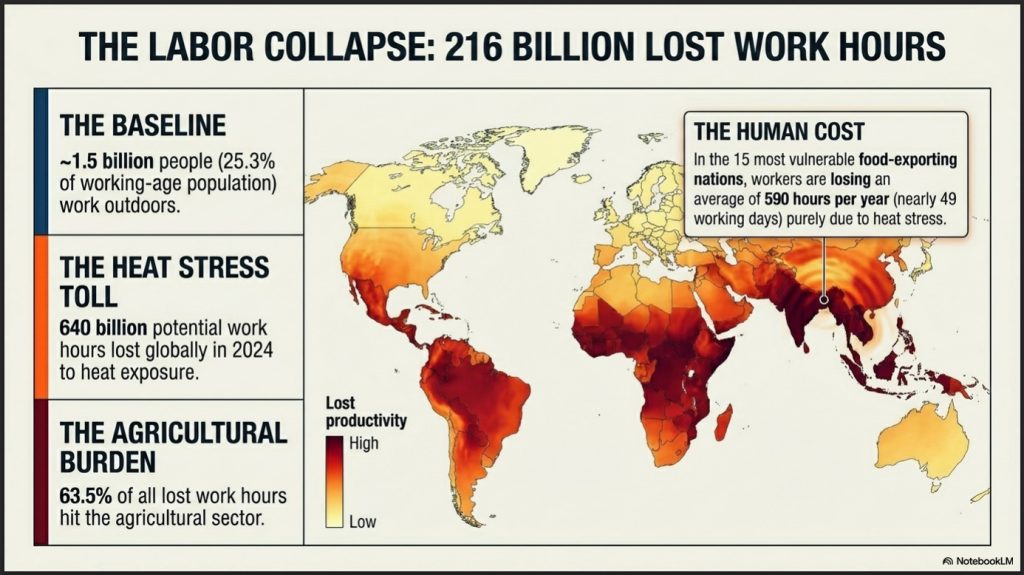

Beyond crop physiology, the human cost is a primary driver of supply contraction. In 2024, the global agricultural workforce lost 216 billion potential work hours to heat stress—averaging 590 hours per worker in vulnerable nations. This loss of labor capacity, combined with “teleconnections” that cause simultaneous crop failures across multiple continents, prevents the usual market correction where one region’s harvest compensates for another’s failure. These production shortfalls and labor losses translate directly into the financial pressures felt at the British supermarket checkout.

4. The Economic Toll: Food Prices and the UK Consumer

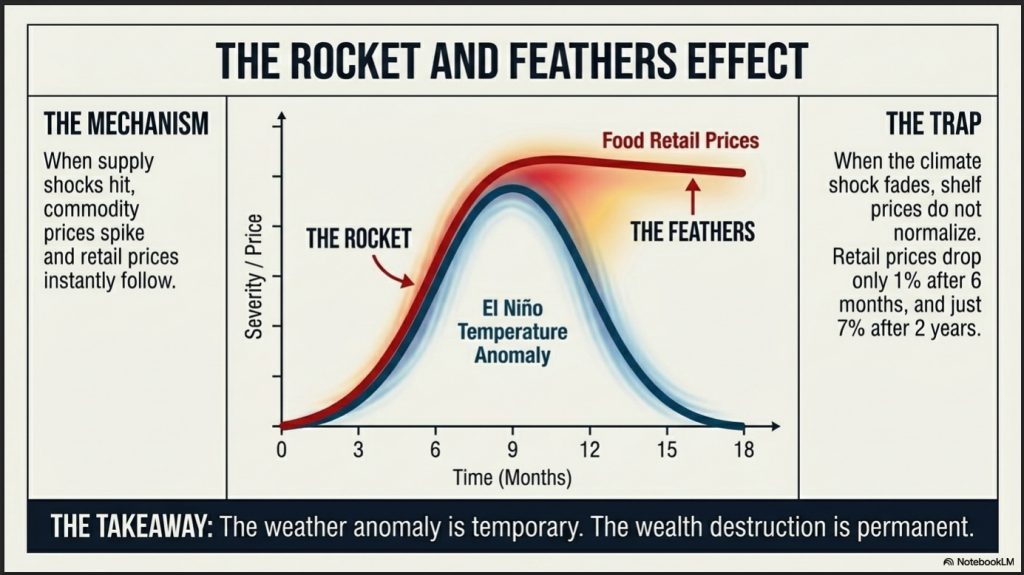

The convergence of El Niño, the Iran War, and energy volatility is driving “structural inflation”—a systemic shift in the cost of basic nutrition. This is exacerbated by the “Rocket and Feathers” effect, where retail prices shoot up rapidly in response to a shock (like a rocket) but drift down only marginally (1-7%) long after the crisis has eased (like a feather). This ensures that even if weather conditions normalize, the price floor for food has permanently shifted higher.

The financial outlook for the UK consumer through November 2026 is critical:

- A projected 50% increase in food prices by November 2026 compared to 2021 levels.

- A compression of historical trends where 20 years of price growth is being packed into just five years.

- Specific and sustained price hikes for staples: Olive Oil (+113%), Beef (+64%), and Eggs (+59%).

These increases are regressive, disproportionately impacting lower-income households who cannot defer food spending. Analysis suggests that the most deprived fifth of the UK population may now be forced to spend 45-70% of their disposable income simply to afford a healthy diet. The 2026 Super El Niño is not merely a weather event; it is a systemic economic shock that threatens to turn basic nutrition into a driver of domestic economic inequality.

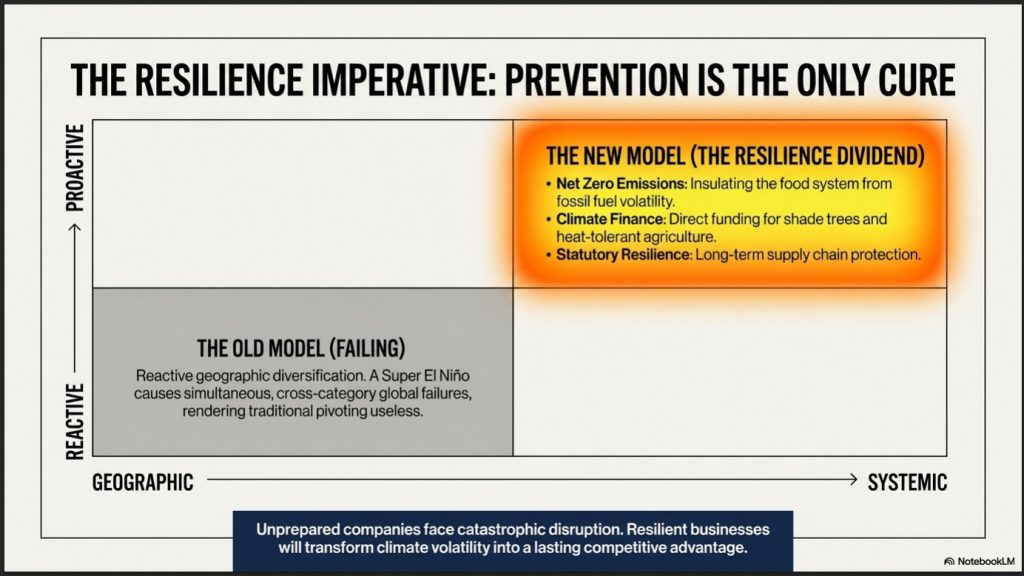

5. Strategic Conclusion and Future Outlook

The 2026/2027 Super El Niño represents a definitive “food system fracture.” The physical mechanics of the Pacific—the surfacing of the Kelvin Wave and the disruption of the Walker Cell—have initiated a chain reaction linking tropical heat stress to British grocery inflation. The combination of simultaneous global crop failures, the labor-suppressing effects of extreme heat, and the compounding price of fertilizer driven by the war in Iran has exposed the fragility of the UK’s import-heavy food model.

To mitigate this, the UK must pursue a “Resilience Dividend”—treating climate adaptation as a strategic competitive advantage. This requires moving beyond reactive crisis management toward structural shifts:

- Pivoting toward “nature-friendly farming” (such as planting shade trees and diversifying crop varieties) to reduce reliance on gas-based synthetic fertilizers, thereby insulating the food system from Middle Eastern energy shocks.

- Increasing domestic storage capacity for non-perishable staples to buffer against the “Rocket and Feathers” effect of global commodity spikes.

- Diversifying supply chains to avoid geographic concentration in regions where El Niño teleconnections trigger simultaneous failures.

Ultimately, the 2026 Super El Niño proves that prevention is the only effective cure. Without a strategic shift toward resilient agricultural systems, the affordability of nutrition in the UK will remain permanently tethered to an increasingly volatile global climate.